The AI hype is only part of the EU energy story

AI is the accelerant, but the fire was already burning

Last week I wrote about the enormous bill — the European Commission puts grid investment alone at around €584 billion this decade — that EU energy supply and the grid in general has to bear if we are to dream of long-term AI sovereignty.

On the one hand the investments needed are mind-blowing, on the other there is a whole industry already rubbing its hands at the business this inevitably brings. Yin-yang.

Naturally, there are sceptical voices, and they typically take one of two forms. The first says AI — in its current incarnation i.e. LLMs — is a bubble, and a bubble sooner or later pops; when it does, all these investments come to naught, and the problem pops along with it. The second says efficiency will outrun demand: the current architecture — transformers and the hardware under them — will be optimized so aggressively that the mountain of surplus compute we’re racing to build simply won’t be needed.

Personally, I have issues with both lines of argument. On the first: the fact that a bubble pops doesn’t mean the demand shrinks — the dot-com crash bankrupted companies, but demand for the internet grew many times over in the years that followed. On the second: Jevons. We have seen it recently with token costs — they have fallen at least fourfold over the last two years (you could easily make an argument they fell between 10-100x if you take into account fixed capability), and yet we typically pay more than we used to, not less. I wrote about that here.

But let’s put this aside. I am willing to admit that I can’t predict the future with high precision. Time will tell.

And yet, there is another factor that makes both of these lines of thinking likely inaccurate. And the reason has almost nothing to do with AI. More than that — AI is only part of the reason demand is growing at all. Electrifying transport, swapping gas boilers for heat pumps, and reindustrializing the continent each add new load on a scale comparable to data centers. AI just happens to be the fastest-climbing line on the chart.

Let’s get to a different angle. The current explosion in energy demand is just an overcurrent - and the European grid infrastructure, as it is, requires a decade-long investment either way. Even if AI demand gets slashed by half tomorrow.

Let’s walk through five forces reshaping the European grid right now. Only one of them is about AI. The other four would be tearing at the system even if every frontier lab folded tomorrow.

But first, let’s look at the frame that makes the whole thing click.

In general there are two different things we sloppily lump together as “the grid problem.” One is rebuilding — changing what kind of power spins, when energy arrives, and how we store it.

The other is growing — adding raw load. These are not the same engineering project, they don’t run on the same timeline, and crucially, they don’t have the same cause.

The rebuild is forced by the energy transition itself. The growth is forced by electrification — electric cars, heat pumps, reindustrialization, and yes, data centers. AI lives almost entirely in that second bucket. It is a volume driver, and it barely touches the first.

Which is the whole point. If you pop the AI bubble, you remove a chunk of the growth. You don't remove a single gram of the rebuild. And the rebuild is hard, slow, and expensive. Hold that distinction — we'll come back to it.

OK, let’s now get into the five forces I’ve mentioned earlier.

1. The grid forgot how to stay up

Start with the most uncomfortable fact, the one we tend to avoid because it lives in a part of engineering we could have conveniently ignored for years.

On April 28, 2025, at 12:33 in the afternoon, the Iberian grid lost roughly 15 GW of generation in about five seconds — close to 60% of everything that was online at that moment. Voltage surged out of control, and within seconds Spain and Portugal separated from the rest of continental Europe and the lights went out for tens of millions of people. The bill was real: roughly 500 flights cancelled, factories like Volkswagen’s Navarra plant idled, and economic-loss estimates as high as €4.5 billion (more likely though between €1-2 billion).

Here’s the key part. At the moment it failed, the Iberian system was running on over 70% solar and wind through inverters. Even though the eventual root cause was voltage control, not the renewables share, the inverter question still matters — and here is why: inverters don't spin.

A gas, coal, nuclear, or hydro plant runs on an enormous lump of metal rotating at grid frequency — spinning in lockstep at the grid’s 50 hertz, synchronized across the whole European network. That spinning mass is not only a side effect — it’s also a shock absorber. When supply suddenly drops, all that rotational inertia keeps turning and buys the operators a few seconds of physics before frequency collapses. Those seconds are the safety margin: they are the window for fast frequency response from batteries (which can react in well under two seconds) and for governors on the remaining spinning plants to ramp up. Run out of that window and the grid’s last-ditch defense kicks in — automatic under-frequency load shedding, which simply disconnects whole blocks of customers to save the rest of the system.

Solar panels and wind turbines give you none of that for free. (And yes, a wind turbine does have a spinning rotor — but it is connected through power electronics that electrically decouple it from grid frequency, so the system can’t lean on that mass the way it leans on a directly-coupled generator.) Grid-forming inverters — the newer kind, programmed to actively imitate a spinning machine and inject power the instant frequency dips — can synthesize a version of it, but they are a rounding error in today’s deployment.

So you end up with a grid that is cleaner, cheaper to run on a sunny afternoon — and structurally twitchier than the one it replaced. Lower inertia means less margin for error. That fragility is not the whole story of the April blackout — the official inquiries trace the collapse to a cascade of overvoltage and failed voltage control, with low inertia and weak interconnection as aggravating conditions rather than the single trigger. But it is the structural backdrop against which any such cascade now plays out. (Side note: the report quoted here is a genuinely fascinating read — worth at least a cursory look.)

This has nothing to do with AI. It is a property of the energy transition itself. We are swapping spinning mass for silicon faster than we are building the things that compensate for it.

2. We are paying people to take the electricity away

The second force shows up in the price.

In 2025, Poland recorded over 300 hours of negative day-ahead electricity prices — more than double Great Britain’s 149, and on a clear upward march year over year. And remember: Poland is a renewables laggard by EU standards — about 29% of its power came from renewables in 2024, against an EU average near 47%. If a country this far behind the curve is already paying people to take its midday solar, that tells you the imbalance is structural. April alone saw a record run, with roughly 27% of the country’s solar output exposed to prices at or below zero — up from 5% a year earlier.

A negative price means exactly what it sounds like. There is so much power on the grid at midday that producers pay buyers to absorb it. In Poland the tax authorities have actually had to rule on how to charge VAT on the transaction — because someone is rendering a service by taking your electricity off your hands.

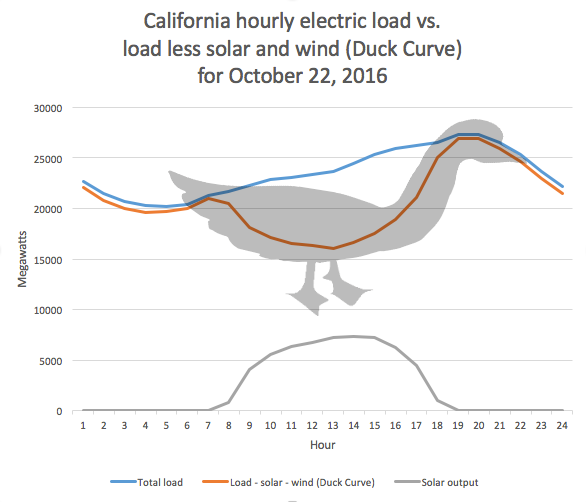

This is the duck curve — plot net demand (total load minus solar and wind) across a sunny day and the line sags into a deep belly at midday, when solar floods in, then rears up into a steep neck in the early evening as the sun drops and everyone gets home. And it is not a victory lap for solar, mind you. We have built enormous quantities of generation that all arrives at the same hour, in a system that still can’t move energy across time. So the Polish operator curtails — in one week before Easter 2025, PSE is reported to have cut around 77.5 GWh of wind and solar — on the order of what the country curtailed in all of 2023. The April picture is starker still: Pexapark puts non-market curtailment at roughly 400 GWh in the first four months of 2025.

Negative prices and curtailment are the grid telling you, in the bluntest language it has, that the system is unbalanced. No AI required so far.

3. Europe is spending billions on batteries

Which is why the third force is the most telling — just follow the money.

In 2025 the EU deployed a record 27.1 GWh of battery storage, up 45% on the year, taking the installed fleet to nearly 80 GWh. Developers are bolting BESS onto existing solar portfolios as fast as they can finance it. And the queue behind that is staggering: by mid-2026, roughly 455 GW of battery projects and 375 GW of generation were stuck in distribution-grid connection queues across eight European markets — around €100 billion of clean assets sitting in a line.

Nobody is putting up tens of billions of euros in storage to power a chatbot. They are doing it because the problem in forces one and two is structural — too much variable generation, not enough inertia, not enough ways to shift energy from the sunny hour to the dark one. Storage is the market’s answer to a physics problem, and the size of the bet tells you how real the operators think that problem is.

4. The geopolitics were here before the GPUs

The fourth force is the one Europe has spent the decade learning the hard way.

Gas dependency. Uranium and fuel sourcing. The critical minerals inside every battery and every transformer. The Baltic states only finished cutting themselves off from the Russian-controlled BRELL network in February 2025, and that single act reshaped storage economics across the region overnight.

So energy security is not a 2026 invention. It is the thing that has been driving European policy since at least February 2022, through a winter of Liquefied Natural Gas (LNG) terminals and price caps and uncomfortable conversations about who controls the molecules. And AI didn’t create that exposure – it just gave us a fashionable new reason to talk about it.

And yet, the dependency didn’t disappear so much as move: the US supplied about 58% of the EU’s LNG imports in 2025 and is on track toward two-thirds in 2026, and Europe has its AI chips, its cloud, and increasingly its molecules sourced from the same single ally — which is its own kind of exposure. Especially in the shifting geopolitical climate.

5. AI is the accelerant, not the fire

So where does AI actually fit?

On top. It lands on a system that was already strained by the first four forces and presses on the timeline. The honest framing is that AI is one input among several, and not even the largest. In other words — it’s the accelerant, not the cause.

Look at the actual numbers and the panic deflates a little (well, AI-induced panic; as some sense of urgency is still truly warranted). Data centers are about 3% of EU electricity today, heading for roughly 4.5% by 2030. AI is only a slice of that — the IEA put AI at around 15% of data-center demand in 2024. So in absolute terms, AI is a low-single-digit percentage of total European load.

The dynamics are more interesting, though. Estimates of how much of the EU’s new electricity demand to 2030 belongs to data centers vary enormously — from around 10% in the IEA’s stated-policy scenario to 20–28% in industry projections. That’s a big share of the growth — but it isn’t even alone there. The electrified industry adds about 80 TWh of demand growth by 2030, electric vehicles around 67 TWh, and data centers around 72 TWh. AI is the fastest-climbing slice of the growth, not the entirety of it.

And for anyone who still thinks EVs are a fad worth discounting: in 2024 pure battery-electric cars alone outsold diesel in the EU — 13.6% of new registrations against diesel’s 11.9% — and in December 2025 they outsold petrol cars in a single month for the first time ever. The fleet is electrifying, whether one likes it or not.

Let’s now bring back the rebuild-versus-grow frame. AI is a growth force. It is responsible for expanding the grid — and it shares even that job with cars, heat pumps, and factories. It is responsible for almost none of the rebuilding — the inertia, the duck curve, the storage scramble. Those came from the energy transition, and they are the slow, expensive, decade-long part.

That distinction is exactly what survives the bubble. If AI demand evaporates, you remove a chunk of the growth pressure — and you don’t get your stable, boring 2019 grid back, because the entire rebuild is untouched. You’d still be low on inertia, still drowning in midday solar, still short of storage, still geopolitically exposed. Same structural crisis, minus one accelerant, with the deadlines nudged out by a few years.

So what does this all mean?

Back to software. None of this is AI’s fault — but all of it is AI’s problem.

Software people carry an instinct that compute scales like software. Need more capacity, spin up more instances, raise another round. But sovereign AI in Europe is no longer gated only by how many GPUs you can buy. It is gated by interconnection queues, inertia limits, and curtailment — a decade-long physical rebuild you cannot accelerate with a term sheet or VC your way through.

That reframes where the hard problems live. If midday solar is free-to-negative and energy storage is scarce, then when and where you run a workload stops being an infrastructure footnote and becomes an optimization problem. Training and inference want to chase the curtailed megawatt-hour — the energy nobody else can absorb — and that is a scheduling problem, a siting problem. In short — a software problem.

OK. So compute doesn’t get to escape the grid. It has to become grid-aware. My take is that we’ll also see some companies specializing in carbon- and price-aware scheduling — deciding which data center wakes up when the wind blows in the right country. By the way this isn’t hypothetical: Google has been running exactly this kind of carbon-intelligent scheduler since 2020.

Full circle, then — to the real connection to sovereignty. The power bill itself was part of the problem. The grid that issues the bill is being rebuilt for reasons that predate the first transformer block — and anyone who wants to build sovereign AI on top of it inherits that rebuild whether they like it or not.

Last but not least — even if every AI lab folded tomorrow, Europe’s energy story would still be the dominant infrastructure story of the decade. Sovereignty isn’t optional.

It just gets a hell of a lot more headlines when we frame it as an AI problem.